NPS, or the National Pension System, is another promising avenue in India for investment with a retirement focus, flexible in a market-linked plan yet stable in a Government-backed scheme. Over the years, it attracted investor fraternities due to its lucrative tax benefits and handsome returns, and a host of new rules that make it more attractive for the common investor to come into this fray. The article presently explores in detail some exciting advantages of NPS, eligibility criteria, and expected return that intrigued many investors’ interests with the introduction of partial withdrawal action. Salient features of the National Pension System:

Source: HDFC life

The NPS is essentially a government-induced pension scheme submitted in January 2004 for all government employees, but it was then opened to all the citizens of India in 2009, including the unorganised sector. It thus follows under the regulative supervision of the Pension Fund Regulatory and Development Authority, and the scheme aims to provide a financial safeguard in old age for all the subscribers.

The National Pension Scheme is a voluntary defined contribution pension scheme whose objective will be to provide a retirement pension. A subscriber can make regular contributions to a pension account during working years. In essence, the scheme offers options for systematic saving and investment in a pension fund over a long period, thus building up a substantial corpus that one can utilise to receive a regular pension after retirement.

Table of Contents

| S. No | National Pension System: Benefits, Eligibility, Returns and New Partial Withdrawal Rule. |

| 1. | National Pension System: Benefits |

| 2. | Eligibility Criteria for NPS |

| 3. | Returns on Investments in NPS |

| 4. | Partial Withdrawal Rule Changes Coming To NPS |

| 5. | Exclusivity of NPS Against Other Retirement Saving Schemes |

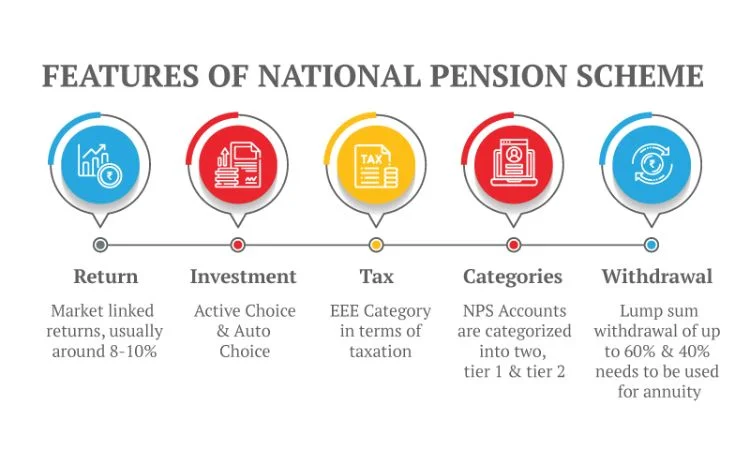

1. National Pension System: Benefits

NPS is an excellent avenue of investment for people planning retirements, as it offers a host of benefits. Following are some of them:

a. Attractive Tax Benefits

Among the most cogent reasons one subscribes to NPS is that it offers attractive tax benefits. The amount subscribed to NPS is deductible and enjoys exemption under various sections of the Income Tax Act, 1961:

The primary reduction under Sec 80CCD(1) would be the lesser of 10% of the Salary, i.e., Basic plus Dearness Allowance, or otherwise, it will not exceed 20% of the total income for self-employed individuals. In terms of getting deductions on individual accounts under Sec 80CCE, there is a ceiling amounting to INR 1.5 lakh annually.

Under Section 80CCD(1B) another INR 50,000 over and beyond the amount set up in Section 80CCE can be availed as a deduction against total income accrued to individuals contributing to NPS. Therefore, the aggregate maximum limit stands at INR 2 lakh every year.

Section 80CCD(2): It enables the employer to contribute towards an employee’s NPS account, which would be exempted from taxation, and this deduction has no specific limit in the hands of employees. However, it shall not exceed 10% of their salary, which consists of a basic salary, including a dearness allowance. Moreover, such advantages are distinct from those provided through section 80CCE.

b. Flexibility in Investment Options

NPS allows subscribers to choose from the pension fund manager and investment options. One may opt for either:

Active Choice: Subscriber will have a choice to select the percentage of investment to be done in the asset classes, namely Equity (E), Corporate Bonds (C), and Government Securities (G). The equity exposure for subscribers below 50 years of age could be as high as 75% of the overall corpus.

Default Option: Automatic option for the subscribers who are unwilling or unable to take an active decision. It will automatically determine the allocation for different asset classes concerning the subscriber’s age. While increasing the subscriber’s age, the equity exposure would gradually decrease, and more emphasis could be placed on safer instruments like government securities.

c. Affordable Investment

The NPS happens to be one of the most inexpensive pension products available in the Indian milieu. That essentially means that when compared with other forms of investment alternatives, such as mutual funds, the charges on the funds are at their ebb. Great benefits accrue from this include the contribution invested and growth concerning time, which benefits the investor in the long run.

d. Portfolio diversification investment

These investments are professionally managed by pension fund managers, adding to the diversified portfolio mix of government securities with equities and bonds. The scheme can be risk-spreading without much impact on the saving schemes, which get higher returns than traditional saving schemes.

e. Normal Pension Post-Retirement

The subscriber shall purchase the annuity from a PFRDA-registered and empanelled life insurance company by utilising the accumulated corpus in his account until the age of 60 years for a monthly pension thereafter.

f. Portability

NPS accounts are portable across job locations and employers. They can easily be carried forward with changes in jobs or locations, which is generally not possible in the case of employer-provided pension plans.

Source: Canara HSBC Life Insurance

2. Eligibility Criteria for NPS

The National Pension Scheme has some criteria that should be forthcoming from a person before he/she can be admitted into it.

Eligibility Criteria-Age: An Indian citizen between eighteen and seventy years can open an NPS account.

KYC Compliance: This would imply that one should be permitted to prove his/her identity through documents about their name, address and age. Further, NRIs are free to invest in NPS as well without any hindrance. However, if the individual’s citizenship status changes, his/her account will be closed. No compulsory annual payments will have to be made, but it is necessary that at least INR 1000 is contributed every year to keep the account active.

Source: ET Money

3. Returns on Investments in NPS

NPS returns are linked to performance, p-e, meaning their performance is linked to the underlying assets constituting equity, corporate bonds, and government securities managed by the pension fund manager. The history of NPS investments has been relatively competitive because of the equity part, which has the potential for better returns over a long period.

a. Historical Performance

E: NPS has been averaging between 9% and 12% annually for the last decade in equity investments. Again, it’s about the market-related returns.

Corporate Bonds (C): The return from corporate bonds has dropped somewhere between 8-10% per annum.

On the other hand, the investment in government securities G yielded an annual return of 7% and 9%, respectively.

b. Return Expectations

The broad range NPS has been targeting for expected returns is usually around 8% to 10% per annum. However, these returns are linked to the market and their actual performance shall vary per the efficiency of the prevailing market conditions and selected fund manager.

4. Partial Withdrawal Rule Changes Coming To NPS

The major addition to the National Pension System is a newly introduced regulation concerning partial withdrawal. This new rule regarding partial withdrawal enhances the flexibility for NPS subscribers. Hence, it increases the scheme’s popularity among those needing liquidity before retirement.

a. The Partial Withdrawal Rule – Explanation

Partial withdrawals for specific purposes from the accumulated corpus have been allowed to NPS subscribers by PFRDA. Even partial withdrawals are exempt from levies provided they meet the conditions laid down by the regulator.

b. Conditions for Partial Withdrawal

Withdrawal of up to 25% of the subscriber’s own contributions, exclusive of employers’ contributions, subject to the following conditions of partial withdrawal:

1. Partial withdrawal may be allowed in the Fund for either the marriage of the children of the subscriber, which include legally adopted children, or for their higher education expenses.

2. Construction/Purchase of Residential House: A member may be allowed to withdraw the money from the Fund for the construction or acquisition of a residential house/flat for his residence. He may be permitted to allow such a facility to the other provident fund also up to the extent permissible under this paragraph.

3. Medical Treatment of Critical Illnesses: The same could also be utilized for medical treatment of critical illnesses such as cancer, heart attack, stroke, kidney failure, organ transplantation, etc., either for the subscriber himself or for any one of his immediate family members.

4. To Start New Venture: Subscribed by an individual for starting a new venture/business. 5. Skill Development or Reskilling: Subscribers can make partial withdrawals for training in skills development or in a course that aims at upskilling or reskilling to get a new job.

c. Frequency of withdraws and timing, Withdrawal Restriction

The Subscriber can avail of a maximum of three partial withdrawals during the operational life of the N.P.S. account. There should be at least a five-year gap between two successive withdrawals. However, this will not apply when medical treatments become imperative. Partial withdrawal of subscribers who have been subscribers for not less than three years is also allowed.

5. Exclusivity of NPS Against Other Retirement Saving Schemes

While NPS does possess certain relative strengths when compared with other retirement savings schemes within India, this comparison is best accomplished through strong position; there has been no better comparative analysis of the extent to which NPS has enjoyed a built-in advantage than that taken in stride with other retirement savings schemes of Employees Provident Fund, Public Provident Fund, and traditional pension schemes.

a. NPS vs EPF

- NPS can promise higher returns by X% on a slice of the corpus invested in equity, whereas in the case of E.P.F. this return is fixed.

- Tax Exemption: While both NPS and EPF are tax-exempt, in NPS, further exemption is available through deduction under Sec 80CCD (1B).

- Liquidity: As in the case of the NPS, an EPF allows partial withdrawals only under conditions.

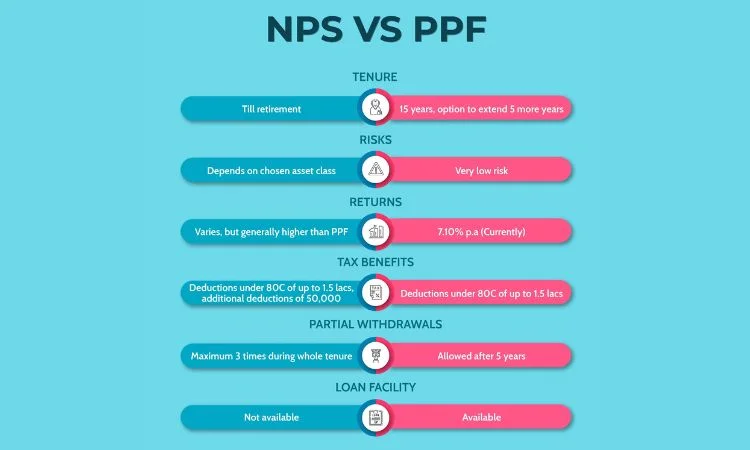

b. PPF v/s NPS

- Returns: They are market-linked and hence way higher returns than the fixed returns by PPF. While retirement ages tagged with a lock-in period are applied to NPS, the lock-in period for PPF account holders is 15 years in consideration. Taxation: All returns on PPF are EEE tax treatment, while NPS is EET tax exemption at accruals and contribution, but it is partially taxed at maturity.

Source: ZFunds

Conclusion

No other investment vehicle offers such a blend of market-linked return, tax benefit, flexibility, and regulative governance. Therefore, NPS is a very attractive choice for planning one’s retirement. It adds a further layer of flexibility offered by the new partial withdrawal regulation, which allows subscribers to unlock funds for specific needs without actually compromising their retirement corpus.

Though NPS has its range of benefits, it is better to think over about one’s risk appetite, financial goals, and the goals of retirement planning before investing in them. This is a growing avenue of investment; hence NPS would surely be able to serve every type of need of an investor and provide the financial security that they want after retirement.