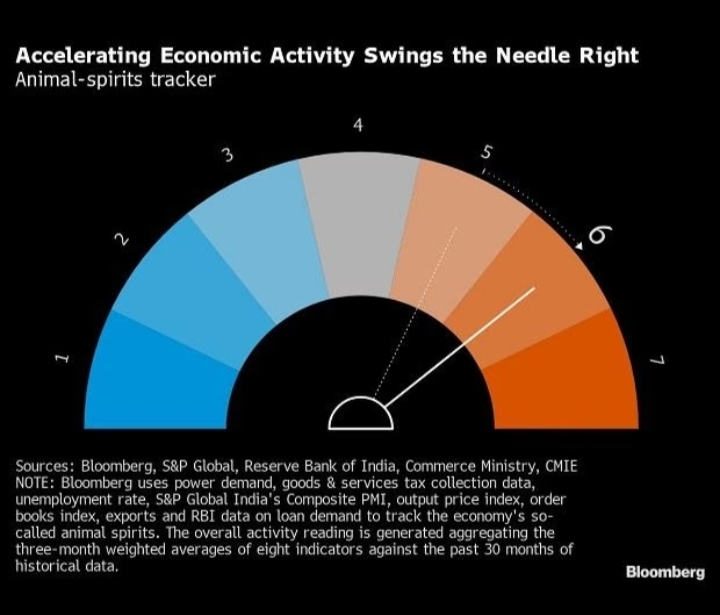

In December, India’s economy showed signs of improvement as business conditions picked up, recovering from a slowdown the previous month. This was indicated by an increase in “animal spirits”, which had remained steady for the previous five months, pointing to a stronger overall economic activity as the year 2022 came to a close.

Increased consumer spending led to an increase in tax collection, and manufacturers expressed positive outlooks for the future. Additionally, the services sector saw growth in new businesses

This report is being released before India’s budget is presented on February 1st, where the Finance Minister is expected to emphasize India’s ability to achieve strong growth in the upcoming fiscal year. The strong performance of India’s economy stands in contrast to many developed countries which are facing economic downturns.

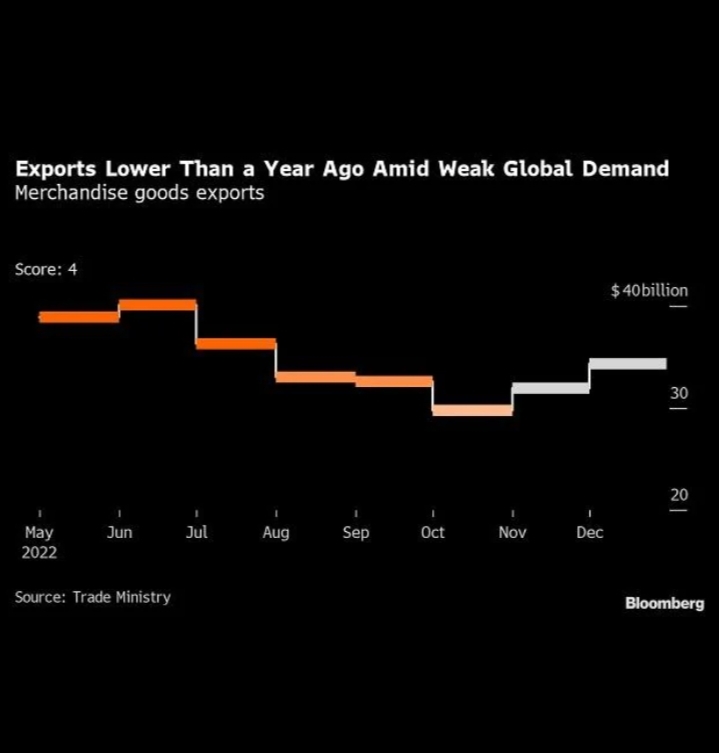

Despite the positive signs, India still has some challenges ahead. Exports have decreased in two out of the past three months, causing difficulties for companies trying to acquire new business from international markets. Prices for finished goods increased as companies passed on increased expenses and costs. Additionally, unemployment in India slightly increased and banks are seeing a decrease in demand for credit among the eight indicators monitored by Bloomberg.

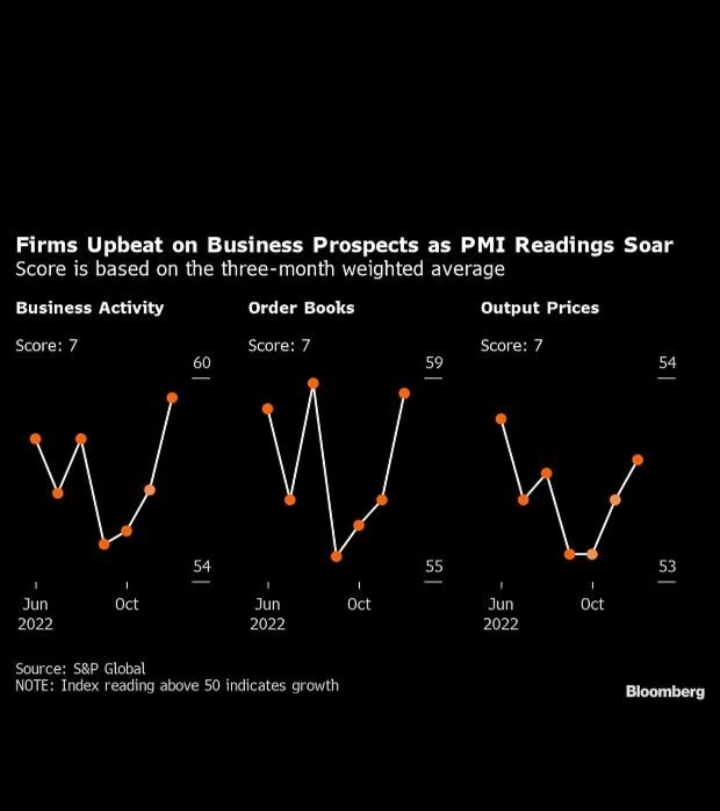

Bloomberg’s animal spirits barometer uses a three-month weighted average to minimize fluctuations in individual monthly readings. The barometer measures various indicators of economic activity, including business activity. According to a purchasing managers survey, both manufacturing and services sectors showed robust activity in December. The composite index reached an 11-year high, with output showing significant growth. In the manufacturing sector, new orders increased at the fastest rate since February 2021, and in the services sector, new businesses continued to rise for the 17th consecutive month in December.

According to Pollyanna De Lima, Economics Associate Director at S&P Global Market Intelligence, “While some may question the resilience of the Indian manufacturing industry in 2023 amid a deteriorating outlook for the global economy, manufacturers were strongly confident in their ability to lift production.” The data on exports showed that it fell 12.2% in December compared to the previous year, but at $34.5 billion it was still at a three-month high in terms of value, as per the data released by the trade ministry.

Commerce Secretary Sunil Barthwal stated that despite global challenges, exports remain competitive. Additionally, imports decreased by 3.46% compared to the previous year, which led to a reduction in the trade deficit for the second consecutive month to $23.76 billion. Lowering commodity prices and a broader decrease in the value of the dollar have helped to decrease India’s import expenses, but continued weakness in exports could impede the recovery from a historically high current account deficit observed during the July-September quarter.

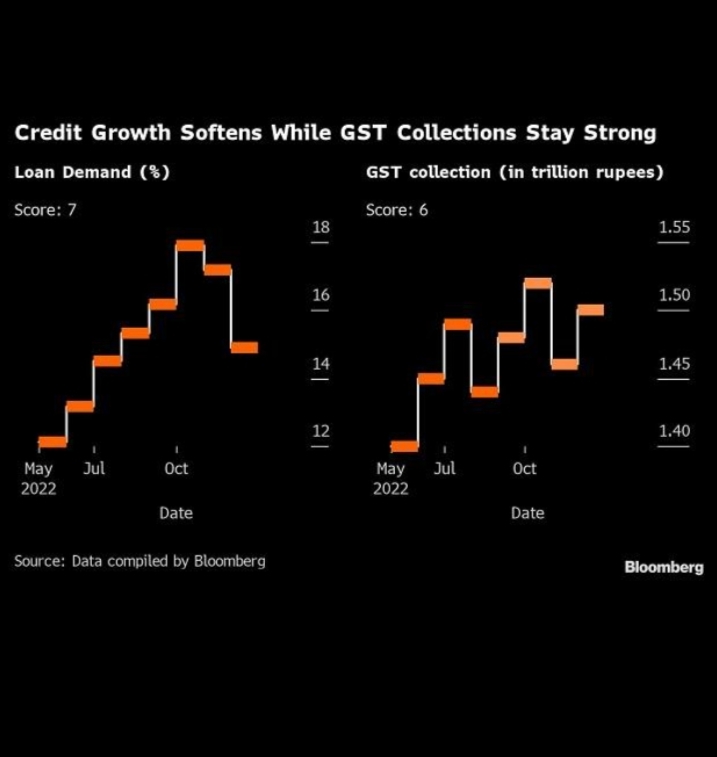

Consumer activity showed mixed signals, as the liquidity in the banking system decreased and bank credit growth slowed to 14.9% in December, compared to 17.2% in November. The Reserve Bank of India’s 225 basis points increases had a dampening effect on demand for housing, automobiles, and consumer goods. However, loan growth of 14.9% is a significant improvement compared to the single-digit expansion seen between September 2019 and March 2022. The collection of goods and services tax, which is used as an indicator of consumption in the economy, increased by 15%. Revenue collection has been consistently more than 1.4 trillion rupees for the past 10 months. New vehicle registrations increased by 8.2% in December, according to data from the Federation of Automobile Dealers Associations.

The market sentiment showed some positive signs, as electricity consumption, which is often used as an indicator of demand in the industrial and manufacturing sectors, increased from the previous month. The peak demand at the end of December rose to 171 gigawatts from 162 gigawatts the previous month. However, the unemployment rate in India climbed to a 16-month high of 8.3%, as job creation was not able to keep up with the expanding workforce.